Supply continues to be the story in our market. But like most blanket statements – “supply is down†– the real picture is always a bit more  nuanced. Supply, like demand, behaves differently depending on the price points. Looking at a broad market overview, active listings counts are down. When active listings decline in the first quarter, the very time active supply should be building, it is a strong signal that supply is weak.

nuanced. Supply, like demand, behaves differently depending on the price points. Looking at a broad market overview, active listings counts are down. When active listings decline in the first quarter, the very time active supply should be building, it is a strong signal that supply is weak.

Not surprisingly, the most constricted inventory continues to be in the 50K-200K range. As Michael Orr of the Cromford Report comments:

“Under $200K, total supply has fallen another 20% since last year, when it was already tight, so buyers looking for homes in this price range are going find it tough going, as they have for a long time now.â€

Perhaps not as predictable, active listings rose in every other price range. That’s right – active listing counts are up in the other prices points! As he continues:

“Active listing counts fell for the price ranges between $50K and $200K, but rose in every other price range. The greatest percentage rise in active listings over the last month was for $800K to $1M which saw an increase of 10%.â€

Does that mean it is a seller’s market under 200K but a buyer’s market in every other price range? No. Again the answers are more nuanced. Although supply is up – so is demand. The growth in demand is exceeding the growth in supply. Increasing supplies are easily being consumed, bringing the supply down compared to last year’s numbers. The Cromford Report continues:

“Between $200K and $2M, supply is down about 10% compared with this time last year. However demand has grown much more strongly for the $200K to $600K range than above $600K, so the balance in the market favors sellers under $600K but is more balanced above $600K.

Over $2M, we have roughly the same supply as last year, which is to say, far more than adequate. In most areas it is a buyer’s market in this top end with the sales rate a little weaker than a year ago.â€

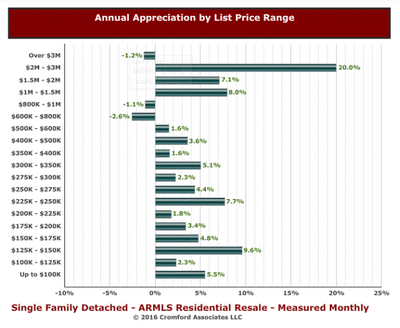

So far closed sales are running about 12% over last year. But the under contract numbers are only up by approximately .4%. Does that mean demand is weakening? Perhaps, but more likely the numbers are being constrained by the lack of inventory where demand is the highest. Buyers shopping in the 200K and under range are frustrated trying to find a home that doesn’t have multiple competing offers. As supply in this price range continues to evaporate, that demand is looking less and less likely to be fulfilled. Not surprisingly appreciation, particularly in the lower price ranges, continues to climb.

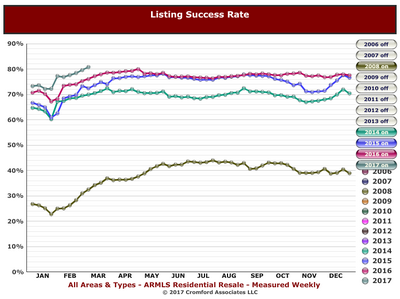

Perhaps the clearest indicator of a healthy market is the “listing success rateâ€. This is the percentage of homes that will sell while listed. The market average seems to hover around 70% in a reasonably healthy market. As a point of comparison, the listing success rate in 2008 (we shudder recalling) hit a low of 22.8%. Right now the listing success rate is soaring. At the moment, traditional home sellers priced under 200k are experiencing an 88% success rate. HUD & REO (foreclosed) homes in the price range are experiencing 100% & 96% success, respectively.  500K and under homes are succeeding at an 83% rate. Numbers this high haven’t been seen since 2013 when the mix of the market was largely distressed sales.

In short, overall we have a very healthy market. Wondering about the specifics of your neighborhood? We are happy to provide a supply demand analysis tailored to your home.

Russell & Wendy

(mostly Wendy)