Author: Russell Shaw

2019 Comes to a Close

As we head towards the end of the year, the market seasonally follows a pattern that tends to favor buyers. Typically between September and  December, active listings grow as demand cools. This year is no exception – although the impact is a gentle one at the moment.

December, active listings grow as demand cools. This year is no exception – although the impact is a gentle one at the moment.

2019 was an interesting year. It began with the market heading towards balance – something we hadn’t seen in a while. But by the end of February, it reversed course and began to strengthen on the seller’s side. June, July, and October produced fewer new sellers coming to market. In fact October set records on the scarcity of new sellers. This dearth of new listings has kept the market favoring sellers, and the seasonal shift has only slightly mitigated that power.

Price

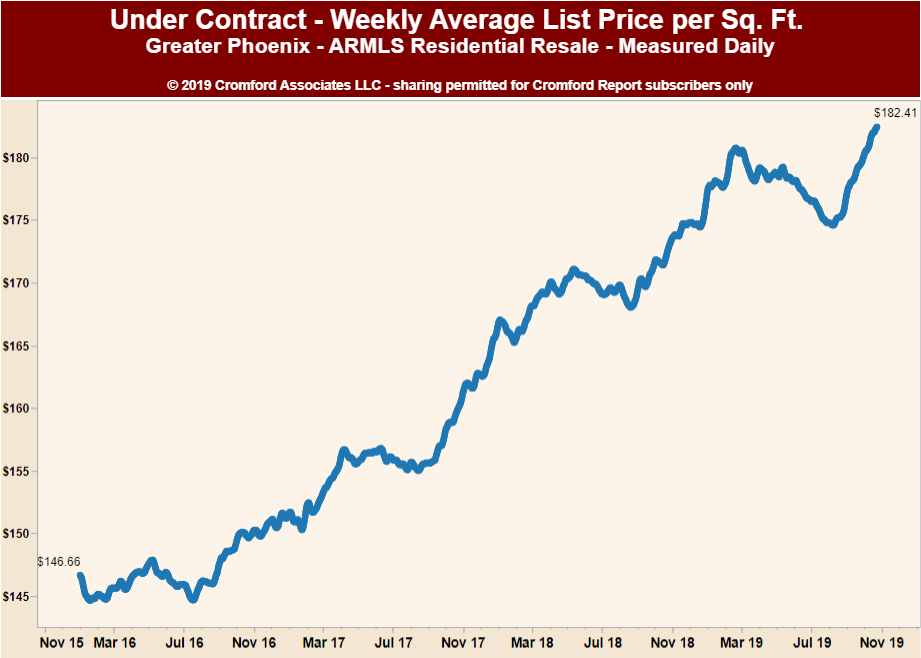

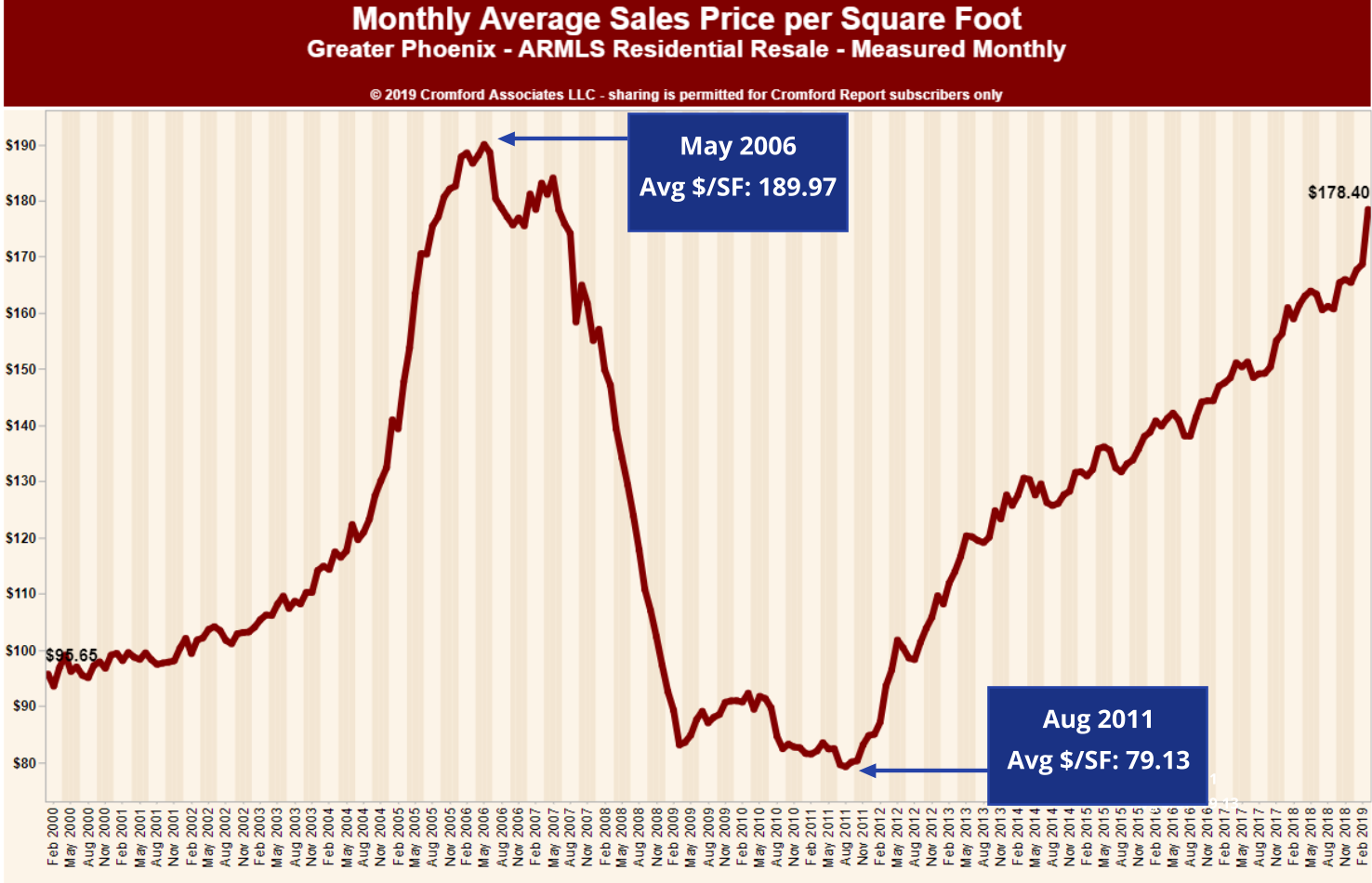

Typically the most interesting thing to real estate buyers and sellers alike, is price. Pricing is a trailing indicator as we have mentioned in the past – often responding 6 months or more to an imbalance of supply and demand. The first place pricing shows up is in list prices followed by pending sales. Price per sq. ft is a pretty reliable indicator. Notice in the chart below how the impact on pricing starts to show up mid – August, literally 6 months after the market shifted in favor of sellers.

As Michael Orr of the Cromford Report comments “This was looking weak during the second and third quarters but has perked up dramatically since August 7…. $181.97 is the highest we have seen since the bubble year of 2005.”

He further comments: “Price momentum is rising, and in normal markets this tends to bring the market closer to balance. It does this by giving sellers better reasons to sell and giving buyers greater affordability problems.” When will the market shift in to balance? That is anyone’s guess but 2020 could be the year.

Bubble

Like any financial market, real estate is subject to two key emotions – fear and greed. When pricing escalates the initial euphoria often gives way to unease. One can hardly blame residents who survived the valley’s market debacle for assuming rising prices equates a bubble. How does one accurately differentiate a bubble from a rising market? Again, Michael Orr provides succinct insight:

“Higher prices should encourage more sellers and discourages buyers which will eventually have a balancing effect on the market. If you ever see that higher prices encourage buyers to buy more, that’s when you have a bubble developing. This is what happened in 2004 and early 2005, but it is not happening now.”

We repeat, a bubble is not happening now. For those who like more in depth analysis of pricing, continue on with Tina Tamboer’s comments:

“The news media is filled with short-term predictions regarding the economy and how it will, or will not, affect real estate prices. It’s understandable for buyers to want their home to appreciate in value after they purchase, who doesn’t? However there is far too much attention paid to short-term influences and fluctuations these days and not enough attention paid to the long view. Real estate is a long-term investment for many people. Despite the euphoria of 2005-2007 and the nightmare of 2008-2011, on average homes are selling 81.6% higher today than they were in the year 2000. That’s an average appreciation rate of 4.3% per year over the course of 19 years. Smaller homes appreciated the most over time while larger homes appreciated the least. Homes under 1,000 sf have appreciated 122% since 2000, an average of 6.4% per year. Those between 1,000-2,000 sf appreciated 106%, an average of 5.6% per year. 2,000-3,000 sf appreciated 68% at 3.6% per year. 3,000-4,000 sf appreciated 49% at 2.6% per year and homes over 4,000 sf appreciated 11% at 0.6% per year.

In short, we are in a normal seller’s market. We expect to see prices rising throughout at least the first quarter of 2020 – if not longer. We will follow the numbers and keep you posted as they unveil.

We thank you for allowing us to assist you with your real estate needs in 2019. We consider it our duty to advise and inform our clients – whether that means buying, selling, or staying put. We wish you and those you love a very happy Holiday season. Here’s to a terrific 2020!

Russell & Wendy Shaw

(Mostly Wendy)

Supply Tightens

In our last paper we discussed demand and its strong rebound (up 8%) from 2018. But we didn’t expound upon the supply side of the story. We will now attempt to remedy that. While demand is more elastic (and therefore perhaps the sexier story) supply might actually be the buried headline.

now attempt to remedy that. While demand is more elastic (and therefore perhaps the sexier story) supply might actually be the buried headline.

The valley has been chronically low in supply for so long that it has become somewhat normalized – but it isn’t normal. As of the writing of this article, residential properties actively for sale are at 17,460 (and only 13,241 without offers). To put that in perspective, average supply would be just under 30,000. While we have certainly seen more extreme past markets such as in 2005 (8,342 active) this low supply is putting tremendous pressure on buyers trying to find properties. It isn’t just the increased demand that is causing the issue – it is also the dearth of sellers coming to market. June 2019 was the second lowest new listings to market for a June since the Cromford Report began tracking it in 2001. July 2019 was the lowest July recorded for new listings. August, the second lowest August. To quote Michael Orr of the Cromford Report:

What is unusual is that supply is 43% below normal. We have had supply below normal ever since May 2011. But the weak flow of new listings has exacerbated the situation.

Does this mean prices are skyrocketing? Perhaps surprisingly to most, the answer is not yet. To understand why Michael Orr further explains:

Pricing is showing no excitement whatsoever, behaving as if the market was normal. This cannot last. Remember that sales pricing is a trailing indicator, often as much as 12 months behind the leading indicators. We expect to see fireworks in pricing over the next 12 months. In fact the current situation reminds us of 2004. The huge imbalance between supply and demand and the absence of distressed properties are very similar.

Now before you scream in fear that if this year resembles 2004, then we are just a year or two away from another housing meltdown, read on:

The big difference is that 2004 was seeing large price increases and a significant number of the homes were being bought for resale by speculative investors and remained empty. The level of mortgage fraud in 2004 was also extraordinary. Hopefully that is not the case in 2019.

These are very interesting times, unlike the past 5 years which were stable and predictable.

Interesting indeed. In fact this year began headed towards a balanced market and has now evolved in to one of the best seller markets in 13 years. But no market lasts forever. Supply and demand are constantly in flux.

What affects demand? The factors are interest rates, affordability, inbound relocation, income/employment, lending practices (i.e. strict vs. easy), population growth, consumer sentiment. It is noteworthy that the millennials have overtaken baby boomers as the largest US adult population.

What affects supply? New builds, equity (positive and negative equity), foreclosures, outbound relocation, personal events (divorce, illness, tragedy, job loss), conversion to rentals or Airbnb, homeowner tenure, consumer sentiment.

How the factors affecting supply and demand will play out is anyone’s guess. We do expect demand to cool in the last quarter as part of our normal seasonal patterns. This should stabilize supply until we arrive at our next spring buying season in February. Pricing of course, will respond to these two factors and affect them as Michael Orr points out:

Once prices have increased sufficiently then we can expect a cooling of demand will follow and the market will start to move towards balance again. No market can stay unbalanced indefinitely.

As always, we will keep you posted as the future unfolds.

Russell & Wendy Shaw

(Mostly Wendy)

Learning from Zoos: 11 Brilliant Mental Exercises for Your Dog

Please click this link to read the article: https://yourdogadvisor.com/zoo-mental-exercise/

~ Article courtesy of Jo, Editor at Jen Reviews

Record Breaking Market?

“This is now an exceptionally strong market with no sign at all of the weakness we were seeing between September and February.” Michael Orr of  the Cromford Report

the Cromford Report

If you are someone who prefers headlines over articles, the above quote summarizes the valley’s current market. For those who prefer more details, read on.

We entered 2019 with sluggish demand that had taken root in the final quarter of 2018. All signs and numbers supported the fact that we were headed for a balanced market. That is until March of 2019 when demand awoke and began reversing trends with vengeance. So what is driving this demand? We can only speculate but there are certainly some likely suspects.

Interest rates Interest can impact the market as they directly affect affordability. By November of 2018 Interest rates hit an average 30-year mortgage high of 4.94%. Fast forward to March and rates had come down almost 1%. As of this writing they are in the 3.75% range. That increases buyer’s buying power considerably and certainly seems to be fueling this demand.

Rental rates When it is cheaper to buy than to rent, the first time home buyer market jumps. This is incredibly impactful as the first time buyer drives the housing market – creating a domino effect allowing for their home seller to in turn purchase their next move up home, and so on with an average chain of seven sales. It is easy for headlines to skip the rental market and focus solely on the resale market but the valley’s rental market is noteworthy. To quote the Cromford Report:

“In June, the average monthly rent per sq. ft. was $1.01 for listings closed through ARMLS. This [is] the first time we have recorded a figure over $1.

In June 2006 the average monthly rent was only 71 cents per sq. ft., so rents have increased by 42% since then. In comparison the average purchase price per sq. ft. has moved from $188.53 to $172.02 since June 2006, a fall of 9%.So average rent has increased 42% while purchase prices have fallen 9% since June 2006 on a cost per sq. ft. basis.”

Job market The valley‘s long term job creation averages around 40,000-50,000 new jobs yearly. However 2018 saw a jump in new jobs to 86,800 according to labor statistics. In fact only Orlando had greater job growth in 2018. Jobs bring people and people need housing. Simple.

Affordability We may get eye rolls with arguing for affordability in a market that has seen such a strong recovery in pricing and appreciation since 2011. But it is worthy to note that Phoenix is the 5th most populous city in the country. Our median sales price of $279,000 is unheard of in cities of our size.

What about supply? We would be remiss to not comment on the other half of the supply/demand equation. Supply hasn’t been abundant for years, so it is easy to dismiss low supply and focus solely on volatile demand. But factually, June was notable for the low numbers of sellers coming to market. As Michael Orr of the Cromford Report shares (emphasis added):

“The most unusual change during June was the 8.5% drop in active listings … which lurched from 5.3% higher than 2018 on June 1 to 4.1% below 2018 on July 1. Much of this decline was due to the low number of listings activated during June – 8,731 is our current count, the second lowest number for June since 2001 and down 11% from June 2018. On top of a very busy month for contracts and closings this has caused the supply to tighten dramatically….This is the greatest imbalance in favor of sellers that we have seen in almost 6 years.

Not surprisingly this is pushing up pricing. As the Cromford Report further reports:

…The monthly median sales price of $279,000 is a new record high. The annual median sales price is also at a new record high at $268,000.

But before you celebrate (or begin having sleepless nights over another “bubble” in housing) there is a secondary set of numbers that typically are more accurate on tracking value. Read on…

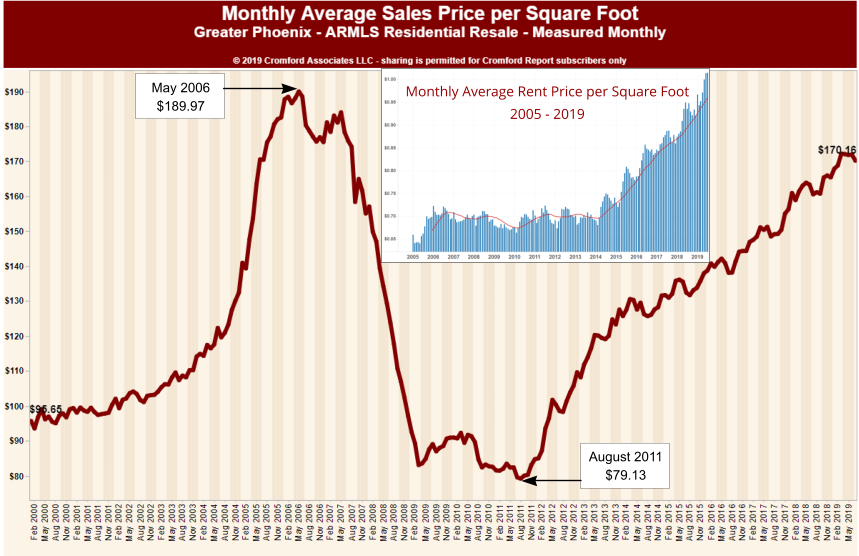

Average price per sq. ft. is nowhere near setting a new record, because the homes being sold today are much larger than those being sold at the last peak. The monthly average $/SF record is $190.05 set in May 2006. We edged up very slightly to $172.30 from $172.01 during June.

There are no indications we are in a bubble. Rather, we simply have a very strong sellers’ market underway. Will it last? History says no. Supply and demand are a seesaw that affect each other. Short supply causes prices to rise. As prices rise, demand tends to falter allowing for a rebalancing of supply. The question is when. As always, we will continue to report the market trends as they unfold.

Russell & Wendy Shaw

(mostly Wendy)

April Showers Bring May Flowers

The strongest time of year for the valley’s real estate market is typically our “spring buying season” – March through May. This year is no exception – but it could have been. We ended 2018 with a rather lackluster market due to anemic demand. Entering 2019 it looked like the market was heading towards a balanced market – something we haven’t seen in the valley for years. But buyers suddenly reversed course and began to enter the market place in strong numbers. What turned things around? Two financial factors: interest rates & raised loan limits.

have been. We ended 2018 with a rather lackluster market due to anemic demand. Entering 2019 it looked like the market was heading towards a balanced market – something we haven’t seen in the valley for years. But buyers suddenly reversed course and began to enter the market place in strong numbers. What turned things around? Two financial factors: interest rates & raised loan limits.

have been. We ended 2018 with a rather lackluster market due to anemic demand. Entering 2019 it looked like the market was heading towards a balanced market – something we haven’t seen in the valley for years. But buyers suddenly reversed course and began to enter the market place in strong numbers. What turned things around? Two financial factors: interest rates & raised loan limits.By April 4th the average 30 year mortgage rate had dropped to a 15 month low. Combine that with loan limits rising (conforming conventional loan limits went from 417K to 484K, and FHA saw a similar bump up) and the buyers responded by buying. As Tina Tamboer from the Cromford Report shares:

“The drop in mortgage rates could not have come at a better time for sellers. Up until 6 weeks ago the negotiating advantage sellers have been enjoying for years in Greater Phoenix had weakened to the point where the market was on track to enter balance within a matter of months and price appreciation would have begun to slow even more.”

But before we break out the party hats, she reminds us:

“Don’t get too excited though, the seller market is still much weaker than last year. Affordability and demand were helped by this interest rate drop but could quickly be negated as prices continue to rise. Sellers still need to be mindful of their asking price to get under contract before buyer activity seasonally begins to decline between May and the end of the year.”

Michael Orr of Cromford Report echoes those sentiments with this:

“We have witnessed a very favorable change in interest rates over the past 4 months and that effect will gradually dissipate unless rates continue to fall even further. Meanwhile prices continue to rise which will re-introduce affordability concerns during the second half of the year.”

The message here seems pretty clear – we are in a sellers’ market, again, and for now. But as the marketplace is a moving target with lots of moving pieces, sellers with a choice may want to pick selling now thereby avoiding the uncertainties of the back half of the year.

Cash offers and seller guarantees

So if the market still remains in the seller’s favor, why would any seller give up their hard-earned equity by taking a “we buy houses” offer? Shouldn’t selling below market occur only in a buyers’ market – where desperate-to-sell sellers are forced to open up their pocketbook to investors? Well, yes, but it would be simplistic to write this off as just illogical human behavior.

Given that we are Realtors with the job of advocating for buyers and sellers, we naturally have a bias against companies that appear to be “helping” in the name of corporate profit. With that said, here are our thoughts – both the good and the bad.

What we like about the “instant offers” or I-buyers:

1. Removes uncertainty. Avoids appraisal and concerns on buyers ability to qualify. Typically will close when the seller wants.

2. No showings, no need to prep the home for sale.

3. The largest one of them allows the seller to cancel the contract with no cancellation fees. Please note: others charge a cancellation fee. Make sure you know what the offer says before you sign.

What we don’t like about the “instant offers” or I-buyers:

1. Below market offers. Home sellers are giving away $20,000 – $30,000 or more of their equity. Most home sellers have no idea that they are taking a below market offer because they don’t know what their home’s true market value is.

2. The home owner is not being represented. The average seller sells every 11 years vs. corporate experts who buy daily. Knowledge is power.

3. Misleading advertising. They claim “No commissions” but charge 6-12% “customer experience fee”. They advertise an “as-is” sale and then typically charge 10k for repairs. They advertise their offers are “fair” when it is below market (“click here for a 15-20% below market offer” doesn’t make for a compelling marketing slogan)

4. Not all homes qualify.

The solution

Change is inevitable in market places. Amazon has changed forever how people buy (ask mall owners). We are not opposed to progress, we embrace it. For our customers (and you need only call or email us to become a customer) we offer a hybrid solution. If you wish to take an I-buyer or investor offer, we will represent you at no cost to you. We have established alliances with the largest investors in town so that we may do that for you. We will explain the costs and your options so you make the choice that is right for you. You don’t have to go it alone.

Russell & Wendy Shaw

(Mostly Wendy)

The Spring Market Awakens

After a slow and non-spectacular beginning to the year, the market appears to be finally waking up. March heralds the beginning of the spring buying season – so

prognosticators watch closely for signs of market health. In the valley the supply side of the economic seesaw (supply & demand) has been fairly stable, if persistently undersupplied. Supply changes tend to be slow moving. Demand, as we have mentioned in the past, can change far more quickly. Jitters were set off in the last quarter of 2018 when the erosion of summer demand persisted. The erosion should not have been shocking given the hit affordability took both in years of rising prices combined with a rapid rise of interest rates. As Tom Ruff in the ARMLS Blog so brilliantly explains: “The decline in year-over-year sales volume began in October as interest rates rose. Adding angst to the problem, employees saw their 401(k)s shrink as the Dow Jones Industrial and the S&P 500 indexes fell 18.8% and 19.6% respectively between the first of October and Christmas Eve. Attempting to soothe nerves, the federal government shutdown from December 22 thru January 25. Happy Holidays everyone! “

prognosticators watch closely for signs of market health. In the valley the supply side of the economic seesaw (supply & demand) has been fairly stable, if persistently undersupplied. Supply changes tend to be slow moving. Demand, as we have mentioned in the past, can change far more quickly. Jitters were set off in the last quarter of 2018 when the erosion of summer demand persisted. The erosion should not have been shocking given the hit affordability took both in years of rising prices combined with a rapid rise of interest rates. As Tom Ruff in the ARMLS Blog so brilliantly explains: “The decline in year-over-year sales volume began in October as interest rates rose. Adding angst to the problem, employees saw their 401(k)s shrink as the Dow Jones Industrial and the S&P 500 indexes fell 18.8% and 19.6% respectively between the first of October and Christmas Eve. Attempting to soothe nerves, the federal government shutdown from December 22 thru January 25. Happy Holidays everyone! “

We could not have stated that better.

The “sky is falling” predictions of prices dropping, however, have no economic basis to them. That happens only after time in a buyer’s market. We repeat, we remain in a “gentle” seller’s market. In fact, despite the sluggish start – demand is picking up steam. So naysayers predicting a buyer’s market or drop in prices will likely have to wait beyond this year. At least in the valley. The proof is in the numbers as evidenced by Michael Orr of the Cromford Report:

The market started the year far behind 2018 in terms of demand – the monthly sales rate was down 11% on January 1 from a year earlier while the count of listings under contract was down 17%. At the end of January these numbers had changed to down 17% and 14% respectively. At the end of February they had changed to down 8% and 12% respectively.

What can we conclude from this? First, we know the under contract count is a leading indicator for closed sales. The 17% gap at the start of January suggested that January closings would be weak and they were indeed, down 17%. The slight improvement in under contract counts to 14% down suggested a mild recovery in February. We actually saw an even stronger recovery to just 8% down. This is quite respectable when you consider that because pricing was up year over year, the dollar volume in February was $2,127 million, not far (2.6%) below 2018s $2,184 million.

At 12% down compared with last year, under contracts counts are recovering from 17% and 14% down at the beginning of the previous 2 months. We anticipate that March sales will reflect that recovery and it is possible that the sales gap could narrow further, even enough to close the dollar volume gap completely. This assumes that current trends continue, which is not certain, but reasonably likely.

Not all areas were impacted equally. Phoenix and Central Valley fared the best (down 2.4%) and the Northeast Valley the worst (down the 4.7%). All in all – not much to fret about. To quote Mark Twain ““The reports of my death are greatly exaggerated.” And so it is with our market. As always, we will continue to keep you informed as the trends solidify for the year.

Russell & Wendy Shaw

(Mostly Wendy)

2019 Market begins with a whimper

2019 began with an unremarkable start. Not surprising given that the last two weeks in December saw a large drop in listings under contract (a drop of 18.5%  compared with the first two weeks of December – and down 10% for the month compared to December 2017). To quote Michael Orr of the Cromford Report “In every respect, December was a weak month for demand, the weakest December we have seen since 2014 for sales … We have not seen listings under contract this low on January 1 since 2008. Clearly buyers are unenthusiastic about buying homes compared with just a few months ago.” In fact, for those who follow our market updates, we had reported that buyer demand first began wavering as early as July 2018. Rising interest rates combined with higher housing prices impacted affordability, putting a gentle damper on demand. But, before we all panic, there is counter balance on dropping demand. The valley is blessed with positive net migration (i.e. population growth) which is still exceeding the current supply. So the real question is what will win in the spring buyer season? Buyers diminished appetite or the inflow of new buyers? Stay tuned, we will have that answer for you in a month or two.

compared with the first two weeks of December – and down 10% for the month compared to December 2017). To quote Michael Orr of the Cromford Report “In every respect, December was a weak month for demand, the weakest December we have seen since 2014 for sales … We have not seen listings under contract this low on January 1 since 2008. Clearly buyers are unenthusiastic about buying homes compared with just a few months ago.” In fact, for those who follow our market updates, we had reported that buyer demand first began wavering as early as July 2018. Rising interest rates combined with higher housing prices impacted affordability, putting a gentle damper on demand. But, before we all panic, there is counter balance on dropping demand. The valley is blessed with positive net migration (i.e. population growth) which is still exceeding the current supply. So the real question is what will win in the spring buyer season? Buyers diminished appetite or the inflow of new buyers? Stay tuned, we will have that answer for you in a month or two.

Now on to the other half of the equation, supply. The number of active and new listings coming to market – is equally unremarkable. In fact the dearth of active listings has been the saving grace in keeping the market in favor of sellers despite dropping demand. According to the Cromford Report’s numbers – supply is at about 2/3 of what is required for a balanced market. Juxtapose that to the demand index which at the moment is only 12% less demand than a balanced market. So the market remains still slightly in favor of sellers – even if weaker than 2019.

Does a weaker seller’s market mean that prices are on the edge of dropping? No. In fact buyers waiting for that may have a bit of a wait. A balanced market (which again, we are not in yet, much less a buyer’s market) does not cause prices to drop but rather appreciation to slow down and keep more in line with inflation. Admittedly affordability has taken a bit of hit – but we still are remarkably affordable when compared to other large metro areas. The Cromford Report sums up the current market succinctly:

I have started to see a few writers claim that Phoenix is becoming a buyer’s market. I think this is a huge stretch. It is possible that we have forgotten what a buyer’s market really feels like. We have seen a noticeable downturn in demand but that alone does not constitute a buyer’s market.

In a buyer’s market, supply is higher than demand and currently we still have very low supply and little sign of a significant increase on the horizon. The weaker demand is still more than enough to match the current level of supply. Consequently sales prices still have upwards momentum, although this has eased a little since last spring.

I also hear talk of lower prices, but this talk is not referring to closed sales prices. It refers to the fact that many sellers are adjusting their expectations and bringing list prices more in line with market conditions. This is not resulting in closed prices going lower than last year, as we would expect in a true buyer’s market. In fact the average price per sq. ft. for listings under contract continues to hit new highs.

We have become used to a hot, growing market that strongly favors sellers and now that it is cooler, contracting in volume and moderately favoring sellers, we have a tendency to over-react and make more of the change than it really deserves. We have to stay calm and realistic and be guided by the numbers. These numbers look like a cooling off, not a downturn. We experienced a similar, though more severe, cooling off in 2013-2014, but the last significant downturn took place between late 2005 and 2009 and was followed by a 2 stage recovery from 2009 through 2013. There was also a mini-downturn in 2010-2011 which interrupted the recovery but had little lasting significance in hindsight…

Although the market is cooler and smaller than last year, it is not in any significant trouble.

What does this mean if you are a seller? In 2019 you likely need to be more realistic on pricing and you may need to offer more assistance to buyers in need of help with closing costs. If you are a buyer, you may have a bit more strength in negotiations than in years past – but don’t be fooled in to thinking that waiting will save you money.

As always, we are here to answer any questions about your particular housing concerns. We are happy to help.

Russell & Wendy (mostly Wendy)

Luca is a two-year-old long-coat Chihuahua mix

Luca is a two-year-old long-coat Chihuahua mix weighing in at a chunky-monkey 24 pounds. He knows he is an irresistibly foxy boy, and his sweet puppy face  will make you want to reward him with treats just for being so dang cute. Luca will use his looks and charms to get away with whatever he can, just like any typical teenager. He needs an experienced owner who will give him boundaries and structure. He will learn that he is not the one in authority and that by following consistent guidelines set by his owner he can reap the rewards of love and affection. Luca is a smart boy that does want to please. He knows the cue to sit, plays fetch, and enjoys romping with his doggie friends. Luca loves being taken out on walks and he will strut about town. You can meet Luca at Home Fur Good, Thursday, Friday or Saturday between 11 – 4. The shelter is located at 10220 N 32nd Street in Phoenix. His adoption fee is $225 and includes spaying/neutering, age-appropriate vaccinations and microchipping. You can see all the pets available for adoption at homefurgood.org.

will make you want to reward him with treats just for being so dang cute. Luca will use his looks and charms to get away with whatever he can, just like any typical teenager. He needs an experienced owner who will give him boundaries and structure. He will learn that he is not the one in authority and that by following consistent guidelines set by his owner he can reap the rewards of love and affection. Luca is a smart boy that does want to please. He knows the cue to sit, plays fetch, and enjoys romping with his doggie friends. Luca loves being taken out on walks and he will strut about town. You can meet Luca at Home Fur Good, Thursday, Friday or Saturday between 11 – 4. The shelter is located at 10220 N 32nd Street in Phoenix. His adoption fee is $225 and includes spaying/neutering, age-appropriate vaccinations and microchipping. You can see all the pets available for adoption at homefurgood.org.

![]()

Sellers Still Retain Control

Happy New Year! We hope that you had a wonderful holiday season.

2018 closed with a bit of a whimper in the valley as buyer demand, after years of unflinching strength, finally wavered. Demand began to drop in July – rather precipitously by October – before settling in to a gentle landing to end the year. Despite lessened demand and the dreary national headlines to the contrary, 2019 begins in the valley with sellers still retaining the upper hand. To summarize the market conditions, no one says it better than Michael Orr of the Cromford Report:

“The reality in Greater Phoenix is that we have shifted from a strong seller’s market with high volumes to a moderate seller’s market with slightly lower volumes. In due course this is likely to adjust appreciation rates from the 8%-10% level to more like 6%-8%. If the CMI** drops below 120 I would change our prediction to 4%-6% but at the moment there is little sign of a fall much below 130. At a CMI of 100 we would expect appreciation. Of course things could change at any point but it would need a new factor coming into play.

The housing market has seen 3 factors put a slight dent in demand:

- Mortgage interest rates are at a much higher level than in 2017, though still far below long term averages.

- The cost of home ownership has risen faster than rents.

- The tax law changes since 2018 have removed many of the tax benefits of owner-occupied housing relative to renting.

We definitely do not have anything approaching a crash or a slump, which would require a large increase in supply. Supply remains weak because many existing homeowners are more reluctant to move. Doing so would require them to give up their existing cheap loan and take out a new more expensive one. They are tending to stay put, which is good news for the likes of Home Depot and home remodeling and redecorating companies.

Other parts of the country are reporting weaker markets at the upper levels, but in Greater Phoenix, the luxury market is looking strong. Supply of higher end homes is down from last year and demand is holding up rather well. Of course the luxury market in Arizona is priced like the mid-range market in many parts of California. Population flows are favoring Arizona too, so it looks as though Phoenix will have one of the leading housing markets over the coming year, even though it is likely to be somewhat less active than 2018.”

So what is the take-away for sellers and buyers in this market? Despite lessened demand, buyers are still exceeding the chronically low supply leaving most sellers in a gentle seller’s market. The weakened demand is however contributing to more price reductions and a greater likelihood of sellers paying buyer concessions during contract negotiations. For buyers, any plan of waiting for lower interest rates and lower prices will likely result in a very long wait. Even balanced markets typically appreciate at the level of inflation – and it is not likely to be in a balanced market in the first quarter of 2019, perhaps not even in the year. Therefore buyers will still be better served shopping in this gentle seller’s market than waiting for a buyer’s market to arrive.

Of course, neighborhoods and price points vary in their supply and demand. For details on your specific area, please contact us. We are always here to help! Thank you for all your support in 2018. Here’s to a wonderful 2019.

Russell & Wendy Shaw

(Mostly Wendy)

**Cromford Market Index; definition: is a value that provides a short term forecast for the balance of the market. It is derived from the trends in pending, active and sold listings compared with historical data over the previous four years. Values below 100 indicate a buyer’s market, while values above 100 indicate a seller’s market. A value of 100 indicates a balanced market